Why Invest in Private Companies?

Why Invest in Private Companies?

Don't you have enough on your plate already?

Historically, private company investing has been reserved for the privileged few. It’s not hard to understand why: startups carry lots of risk and often require huge sums of capital. The investment process involves price negotiations, costly legal services, and complex transfer requirements. The companies themselves are more difficult to understand than, say, Coca Cola. Early-stage companies, especially in tech, may not own large tangible assets like land or factories, but instead hard-to-value intangibles like intellectual property. A startup may not be acquired or go public for a decade, if at all. Until recently, the asset class just didn’t make sense for those with limited capital, low risk appetites and a need for liquidity (i.e. most people).

Recent developments are changing the dynamic. While private company investing still carries risk and requires a nuanced investor mindset, the asset class has opened up to a much wider audience. Now, investors may be asking themselves how to approach the topic and whether this is a distraction that could cause more harm than good.

The Opportunity

Private market investing isn’t limited to high growth tech or consumer products, but we know many retail investor newcomers are interested in startups, so that’s where we’ll focus here.

The top quartile of the venture capital asset class performs in line or better than comparable assets in real estate, large cap equity, and bonds.

Of course, these benefits come with their own unique challenges and risks. VCs often refer to the concept that one or two companies provide the entire portfolio return, while many of the companies in it fail or underperform. In other words, a few companies succeed and most don’t, resulting in a total loss of capital. On the upside, the ones that work can generate anywhere from 1x to 500x+ returns.

Instead of focusing on the headline venture successes (like Facebook) and failures (like Theranos), it’s better to quantify the risk and rewards of venture capital like an average investor does with traditional markets.

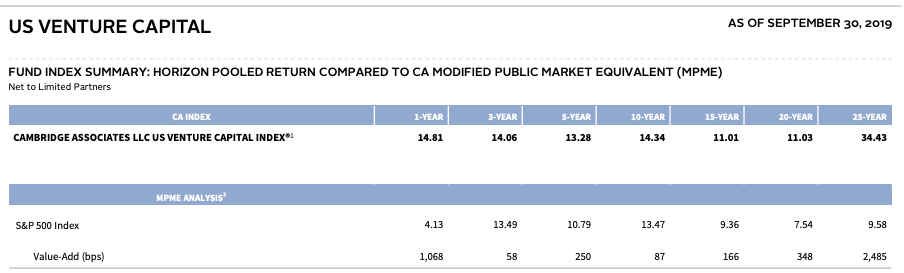

The extreme range of outcomes appears daunting, but venture benchmark returns give some context: The 3, 5 and 10-year annualized IRR for Cambridge Associates’ Venture Capital Index[1] were 14.06%, 13.28%, and 14.34%, respectively. The S&P 500 returned 13.39%, 10.84%, and 13.24%, respectively. The Bloomberg Barclays Credit Bond Index returned 3.16%, 3.61%, and 3.94%.

Source: Cambridge Associates United States Venture Capital Benchmark Book, Q32019

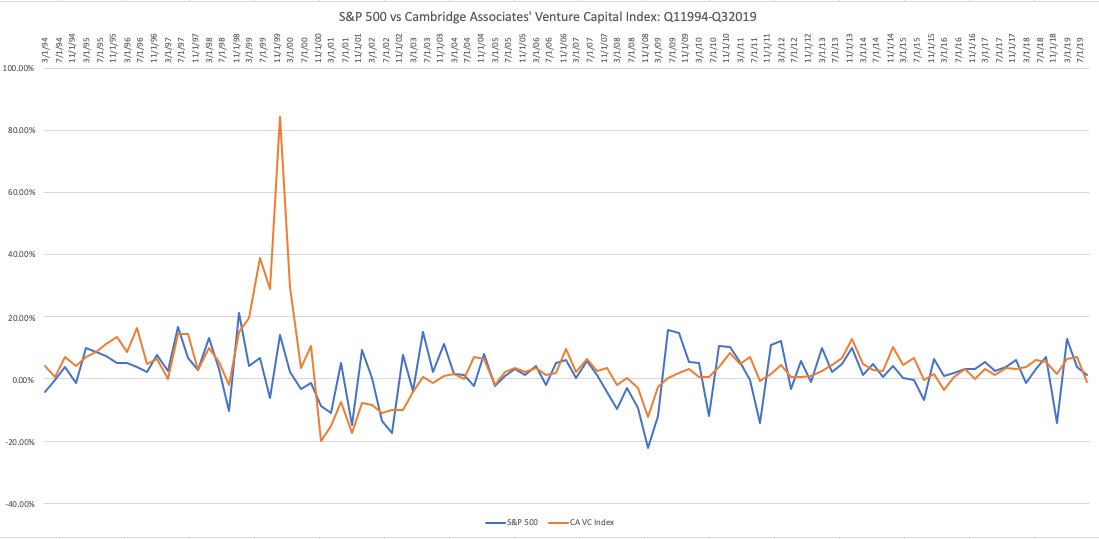

Venture capital’s correlation to public equities is limited, too. Using Cambridge Associates United States Venture Capital Index quarterly returns against the S&P 500 over the past 26 years, we see a low-to-moderate correlation of about 41%.

Sources: Cambridge Associates United States Venture Capital Index, Q32019; Koyfin

This data becomes more relevant as retail investors gain greater access to private markets. The increasing use of secondaries and equity crowdfunding make it so that investors no longer need to write 6, 7, or 8-figure checks to qualify for private company investment opportunities and they no longer need to wait 5-10 years before cashing out.

For example, accredited investors now have access to a number of private exchanges, such as SharesPost, EquityZen, Forge Global and others. Onboarding is more involved than signing up for a T.D. Ameritrade account, but is not terribly difficult. Once approved, investors can access deals on the exchanges and work with exchange representatives to buy and sell share blocks. Many of the listed companies are household names like AirBnB, Stripe, and DoorDash. The shares available usually belong to employees or early investors that, for one reason or another, are looking to exit now instead of waiting for the company to achieve a larger liquidity event in the future. Each exchange has different processes for executing transactions, but the overall trend is that it’s getting easier and less costly to participate.

Equity crowdfunding is an even more accessible avenue that allows nearly anyone to participate in early-stage startup offerings. Platforms such as Republic and StartEngine vet startups and, if approved, place them on their respective platforms with minimum investments as low as $10. Here, investors should understand that these are generally earlier stage companies with limited operating history. Also, there are few, if any, near-term liquidity options. Still, with hardly any barrier to entry and the opportunity to invest at the very beginning of the growth cycle, equity crowdfunding is an interesting option for retail investors looking to participate in private market deals. (We should note that CAPVEE exists to identify and analyze opportunities in the secondary and equity crowdfunding markets!)

Through this lens, we see an asset class that produces as good or better results than public equities and debt, has valuable diversification qualities, has increasing liquidity and more standardized offerings. Investors’ task going forward is learning the process to responsibly and profitably incorporate venture into their portfolios.