*Guest Post* Alphaflow

*Guest Post* Alphaflow

CAPVEE Power-User Reid shares his thoughts on this startup's clever marketplace for real estate debt investing

As you may gather from the header, this week’s newsletter is a guest post from one of CAPVEE’s members, Reid. Reid brought this pick to our attention and wrote an informative, intelligent analysis that we felt needed to be shared with the whole crew. All of our gratitude and big ups to Reid for the contribution!

Summary:

Sector: Platform (Real Estate Investing)

Minimum Investment: $100

Security Offering: Crowd SAFE (Simple Agreement for Future Equity) with $25,000 minimum and $3,930,300 maximum. Deadline of August 15, 2021

Funding Status: AlphaFlow has raised $975,638 during this campaign. Following a record May 2021, CEO noted that he expects to close the campaign out in coming weeks.

Recommendation: Buy; $56.6M post-money valuation; 4.5x potential return

Overview:

AlphaFlow is a unique investment management platform that expands online access to investment in real estate debt. AlphaFlow does this by purchasing residential real estate loans from non-bank lenders. The primary focus is on the bridge loan (“hard money”) market comprised of “fix-and-flip” projects (single-family and small multifamily properties) to then package into portfolios to sell as an investment product to institutional investors. That is a lot… here is an attempt to break that apart:

A bridge loan is (typically) a 6-12 month loan to purchase a property; the loan is collateralized by the property itself (first lien loan). The borrowers for these loans are attempting to fix-and-flip (developer looking to buy, rehab and sell residential properties) property.

Regulation and technological shifts over the past decade have led to massive shift in the residential real estate market towards non-bank lenders. As a result, these bridge loans are typically offered by non-bank entities (i.e. not Wells Fargo). The property developers (borrowers of these loans) trade quick access to capital for a higher interest rate (in the 8%-12% range compared to the 30-year fixed US mortgage rate of ~3%); they want to get started on their project as quickly as possible and cannot wait months to get the loan.

Institutional investors (REIT, Investment Bank, Family Office, etc.) are always looking for higher returns (especially in a low interest rate world) and diversification. Bundling a package of residential real estate loans into a portfolio to then be bought and sold as an investment product is a decades old market. Applying this method to the non-bank fix-and-flip market is a more recent development.

The problem AlphaFlow solves:

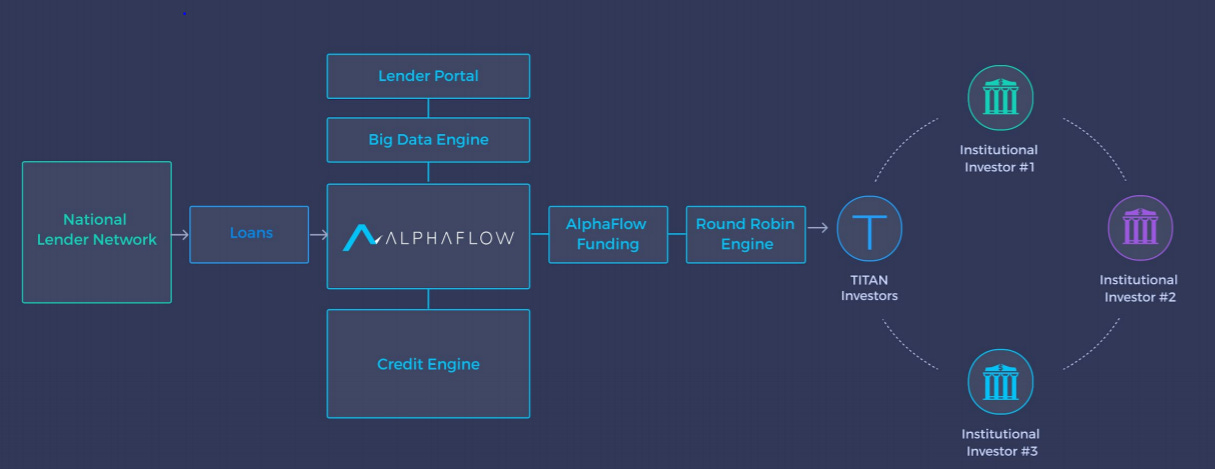

AlphaFlow’s platform connects the market for non-bank loans with institutional investors.

As noted above, lenders in the fix-and-flip space are typically non-bank with a high degree of geographic fragmentation (local lenders serving local communities). The lending process is often manual and lacks quality standards that make it difficult for institutional investors to perform due diligence at scale. Thus, the fragmentation and lack of uniform standards act as barrier to investment for institutional investors.

This is the inefficiency that AlphaFlow seeks to fix. AlphaFlow provides software to streamline and automate manual workflow for lenders, while creating uniform standards in reporting. This software interface for lenders also provides AlphaFlow with strong data on the characteristics of these lenders’ loans, which makes it more efficient for AlphaFlow to determine which loans it would like to purchase. Think of it like a system-of-record for loans that helps bring trust.

Thus, by providing this software interface to lenders, AlphaFlow not only helps lenders to automate and standardize their workflow but helps AlphaFlow itself by aggregating a fragmented lender base onto its platform and accumulating detailed data on loan characteristics to better the loan selection process. This creates a feedback loop with scale that strengthens the platforms value.

Once AlphaFlow has aggregated these fragmented lenders (and thus loans) onto its platform, AlphaFlow uses strict protocols (in the form of algorithms) to decide which loans to purchase. AlphaFlow purchases a loan from a lender, then packages groups of loans into portfolios (diversification lowers risk). AlphaFlow then sells these loan portfolios to institutional investors on the other side of its platform.

By aggregating a fragmented lender landscape for residential non-bank loans, AlphaFlow connects large institutional investors to non-bank lenders. In doing so, AlphaFlow allows these lenders to increase their loan volume (grow their business by providing liquidity to the market) and gives institutional investors the opportunity to invest in a high-yielding market that they have not historically had easy access to. All the while, AlphaFlow is creating a digital system-of-record for the entire industry. By providing liquidity to lenders that lend capital to developers, AlphaFlow’s platform also helps the issue of residential housing supply in the US.

Business Model:

AlphaFlow makes money when it sells loans to institutional investors. For bridge loans sold, AlphaFlow takes a 50 basis point sale premium on the value of the loan sold as well as a ~1% “strip” on the interest rate of the loan (Management notes AlphaFlow earns approximately 1.5% on all the loans it sells to clients). For example, a $500,000 loan would be sold for $502,500 with AlphaFlow taking $2,500. If said loan has an interest rate of 10%, then AlphaFlow will “strip” 1% of the interest on a monthly basis for servicing the loan sold to institutional investors (thus about a 1.5% return).

Loan volume on the platform is an important key performance indicator as AlphaFlow is a platform taking a proportion of the volume as a fee for connecting the two sides of their platform (lenders and institutional investors). At the same time, quality is paramount as the Great Financial Crisis of 2007/2008 showed how foreclosures can be destructive for all parties involved. As such, AlphaFlow uses technological prowess to focus on high quality loans; first lien with loan-to-value ratios at maximum of 75%.

Team:

Ray Strum (Co-Founder/CEO): Ray previously founded RealtyShares, a crowdfunding platform for real estate investing, which was one of the first platforms of its kind. Earlier in his career, Ray worked in investment banking at Bear Stearns and Lazard Freres, as well as a stint in private equity at CCMP Capital. Ray holds a JD/MBA from University of Chicago and a BBA in finance from Notre Dame.

Ray has spent the past ~8 years building businesses in the real estate space, with the past 6 years being dedicated to AlphaFlow.

Nathan Scharfe (VP of Product & Engineering): Nathan was previously Director of Engineering at MoPub before MoPub was acquired by Twitter. While at Twitter, he helped to integrate MoPub into Twitter’s ad offering. Prior to that, Nathan was a founding engineer at IntoNow, which was acquired by Yahoo. He has a BS and MS in Computer Science from Stanford University.

Recent Developments:

Below are a few recent updates and important notes regarding AlphaFlow’s progress:

In early 2020, as COVID-19 shut the world down, AlphaFlow’s business was negatively impacted. Given the magnitude of the economic shock, lenders raised their interest rates and raised equity requirements necessary to qualify for a loan. At the same time, institutional investors like real estate investment trusts (REITs) who are active participants in purchasing loans came under pressure as asset values declined in early 2020. This caused these investors to purchase fewer loans, which decreases the liquidity available to lenders who can then make fewer loans. As a result, activity on the AlphaFlow platform slowed quickly.

To fix this issue, in January 2021 AlphaFlow announced a $100M securitization facility in partnership with Saluda Grade (venture capital investor) that will provide a stable capital base. This facility is akin to a line of credit and provides a stable fund for AlphaFlow to purchase and sell loans no matter the phase of the business cycle.

In November 2020, AlphaFlow raised $10M in Series A preferred financing.

AlphaFlow has announced a new long-term rental loan product that is expected to come to market around the end of Q2 2021. If the residential real estate market slows, people still need housing. In this situation, fix-and-flip developers refinance into these long-term rental loans and fill the property with tenants. This product offering provides a defensive base for AlphaFlow during turbulent market cycles.

Management just announced a strong month of May 2021 during which AlphaFlow reached a $7M revenue run rate (strongest month on record). On the back of these positive recent updates, Management plans to raise a Series B round of financing in the Fall of 2021.

Investment:

The investment is for a SAFE note at a $55M valuation cap. This effectively means you are betting that AlphaFlow will be worth more than $55M in the future.

As noted above, management plans to raise a Series B round in the Fall of 2021. Note that additional financing rounds lead to dilution. Management notes that as of May 2021, founders own ~31% of the equity.

Per PitchBook data, early-stage venture rounds have seen increasing valuations over the few quarters as the market heats up. In Q1 2021, the average US early-stage pre-money valuation was $96.3M, while the median was $40M.

Valuation/Financials:

Management notes AlphaFlow’s market is the $600B of real estate debt that gets done outside of banks every year. The current focus is on the $75B fix-and-flip market.

The May 2021 update noted a $7M revenue run rate for the month. Management further noted an expectation of hitting a $10-$11M revenue run rate by the end of 2021, with the goal of 2-3x annual revenue growth over the next 2-3 years. Using these numbers as the basis of projections, AlphaFlow would reach ~$140M in annual revenue by 2025. Then assuming a 2025 EBITDA margin of 20% based on projections for publicly traded marketplace lenders (Lending Club, Funding Circle, and Upstart), a valuation of $56.6M and a forecasted return of 4.5x is the conclusion. More detail available in the model.

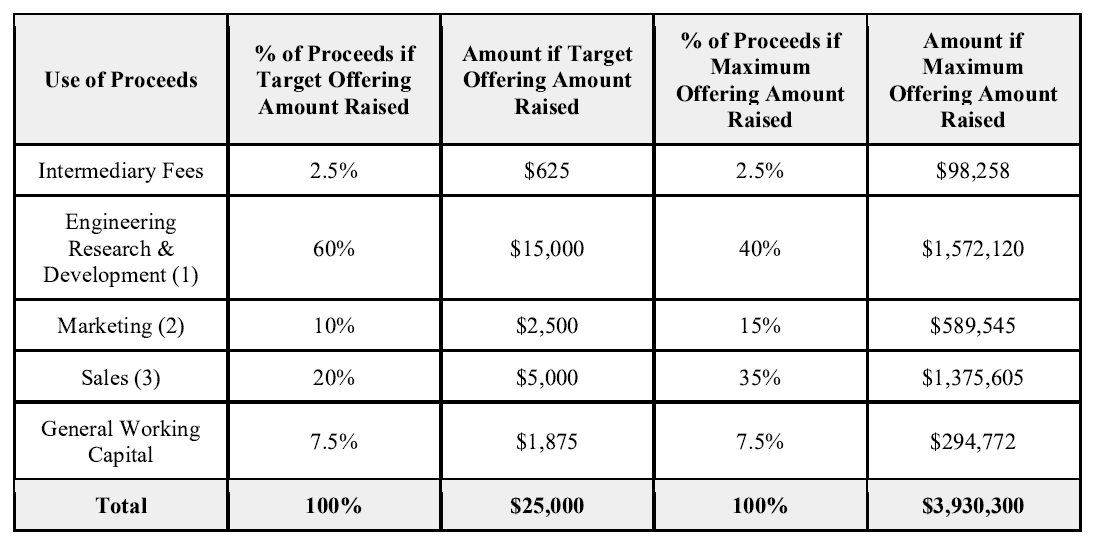

Use of Funds:

Management notes that the funds raised from this SAFE offering will be used for operations and not used to fund loan purchases. The $100M securitization facility will be used to purchase loans to then package and sell to institutional investors. Below is a table from AlphaFlow’s SEC filings detailing the use of funds:

Competition:

Toorak and PeerStreet are noted as AlphaFlow’s main competitors by Management.

Toorak Capital Partners: Founded in 2016, Toorak is a lending platform that funds small residential, multifamily, and mixed-use loans in the US and UK. Toorak acquires and manages loans directly from private lenders that originate loans. Toorak has processed over 15,000 loans since its founding.

PeerStreet: Founded in 2013, PeerStreet offers a two-sided marketplace platform that facilitates investment in non-bank residential real estate debt. PeerStreet raised $60M in a Series C preferred financing round in October 2019; as of that date, PeerStreet had surpassed $3B in loan volume. PeerStreet has prominent venture capital backing with Andreessen Horowitz having led a $15M Series A preferred financing round in 2016.

PeerStreet’s platform is open for investment for both individual and institutional investors. As an individual investor, one can create an account and investment in individual loans (similar to using the Republic platform to invest in individual early-stage companies).

AlphaFlow also competes with other capital markets players (like hedge funds) to purchase loans from originators.

Extra Details:

In SEC filings AlphaFlow notes a $450,000 dispute brought against the firm by a former San Francisco landlord. Management notes their lawyers give no merit to that number; the dispute is a hail mary attempt to get AlphaFlow’s attention.

Positives:

Below are the most important highlights to consider:

AlphaFlow’s management team is top notch. Ray (AlphaFlow CEO) has years of experience in the space as mentioned in the “Team” section; having already built RealtyShares before spending the past 6 years working on AlphaFlow. It appears Ray has built a great team around him, weathered the COVID-19 storm, and AlphaFlow is gaining traction quickly.

AlphaFlow just had a record month in May 2021 and is in good position to raise a Series B preferred round at what should be above the $55M valuation on this SAFE note.

Competitive advantage: in comparison to the competition, AlphaFlow appears to have the superior technology platform. For lenders, the platform allows the lender to run their business and monitor all of their loans (and makes it that much easier to sell them to AlphaFlow); this should provide an advantage in aggregating and maintaining lenders. For investors, the platform provides an easy-to-use system to monitor and track their investment portfolio. At the same time, the securitization facility provides these lenders capital through all market cycles (expect competitors to copy this).

The lenders that AlphaFlow purchases loans from need more capital and have been cut off from many institutional investors. By bridging the gap, AlphaFlow’s platform could help significantly expand the market it serves. This is often the power of successful platform businesses, not only capturing market share but expanding the market itself.

Healthy Skepticism:

Always important to try to think about what could go wrong:

Competitors have strong backing in a competitive space. As noted above, PeerStreet has raised capital from the likes of Andreessen Horowitz and has a head start with lots more loan volume through their platform.

The non-bank fix-and-flip market is prone to downward cyclical swings during slow economic times. AlphaFlow has a strategy around long-term rental loans to balance out potential cyclicality but that strategy has not been tested.

Pockets of residential real estate has moved to non-bank lenders over the past 10 years. Circumstances could lead to the need for more regulation in the industry that could negatively impact AlphaFlow’s business.

Reid’s Recommendation: Buy; $56.6M post-money valuation; 4.5x potential return

Hit us up on Twitter and let us know what you think! We are always happy to hear from you and discuss your questions and concerns.

Disclosure: The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a duly licensed professional for investment advice.