CAPVEE Pick: Insurtech that saves your grandma from getting ripped off

Our take on Gilgal General

Summary:

Company: Gilgal General

Sector: Insurtech

Platform: Wefunder

Minimum Investment: $250

Investment Structure: SAFE ($9.5 million valuation cap)

Funding Status: >$0.1 million ($1.1 million target)

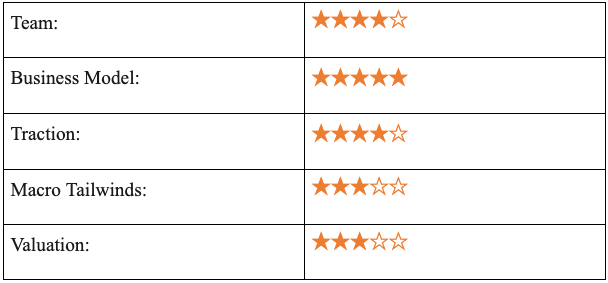

CAPVEE Call: Buy (>14x Return Potential)

Overview

Gilgal General is building the world’s first annuities exchange. Basically NASDAQ for a very specific - and often maligned - financial retirement product.

Before we get into the weeds, let’s quickly discuss what an annuity is.

In its most basic form, an annuity is a contract that guarantees a fixed monthly payment from an insurance company against an upfront fee. Annuities play an important role in retirement planning by helping retirees guard against outliving their assets. There are many types of annuities with key features that include lifetime income, tax savings, and benefits in estate planning.

Gilgal General is planning to launch a beta version of its annuities exchange in Q2 2022 and has already signed-up 8 of the 20 largest insurers in the U.S. as market-makers or clearing-members, ensuring sufficient liquidity on the exchange.

The company was founded by Alexander Ampontuah, a New York-based ex-banker with 20+ years of fixed income trading and risk management experience. It’s backed by an impressive advisory board including Stan Lewis, a top-tier banker at Wall Street heavyweight Goldman Sachs, and Leon Tatevossion, a math professor at NYU. Up until now, Alexander self-funded the project.

The Problem Gilgal General Solves

Annuities are often criticized. They’re sold by brokers and investment advisers to retirees on behalf of insurance companies. Salespeople get a whopping commission of 10% from selling annuities, often in the form of hidden charges and fees. Annuities also charge a hefty early withdrawal fee of up to 10% if you take out your money before age 60. Basically, annuities are purposely confusing and aggressively sold to a vulnerable population.

Gilgal General bypasses brokers and investment advisors as its products can be freely bought and sold on its annuities exchange, which reduces commissions to around 5%. The annuities exchange will also improve liquidity, hence reducing additional transaction costs like early withdrawal fees and contract turnaround time from days to minutes.

The Team

Alexander Ampontuah, Founder & CEO: Alexander is a New York based ex-banker turned financial services entrepreneur. He has 20+ years of fixed income trading and risk management experience at various bulge bracket banks including Bank of America, UBS, Deutsche Bank, and RBC.

Alexander has a BA in Economics from the University of Massachusetts, where he ran varsity cross country and track & field.

Bo Qian, Software Engineer: Bo has 18 years of capital markets technology experience at RBC and Deutsche Bank.

Bo has a PhD in Computer Science from the University of Georgia and a MS in Computer Science from Peking University. He achieved an impressive 4.0/4.0 GPA at both universities, with the notable exception of his mandatory Marxism classes in China.

Cenray Gangadharan, Software Engineer: Cenray has 16 years of capital markets technology experience at RBC, Nomura, and Citigroup.

Cenray has a BS in Computer Science from Kerala University in India.

Alexander and his key software engineers met when they worked together for 5 years at RBC in the bank’s proprietary trading unit.

What We Like

- Gilgal General’s TAM is huge: According to the Insurance Information Institute, the U.S. annuities market was $219 billion in 2020. The market is expected to grow slightly due to longer life expectancy (savers need to invest a larger share of their income to retain a high quality of life and cover living and healthcare costs).

- The financial retirement market is ripe for innovation: According to McKinsey, insurance companies will come under increased pressure to improve productivity. Key trends are automation, digitizing existing high-touch processes, and standardizing products. All of these trends are major selling points for Gilgal General’s annuities exchange solution.

- The timing is right: The 2019 SECURE Act annuity provision permits U.S. employers to carry annuities on workplace retirement plans without incurring fiduciary liability risk. We believe the 2019 SECURE Act will have a significant impact on employees converting a portion of their retirement savings balances to guaranteed retirement income using annuities, much like how the 2006 Pension Protection Act did.

- The solution presents an attractive value proposition for all key stakeholders: The most challenging task will be to get the market participants to adopt this new technology solution in order to achieve the necessary economies of scale and scope.

We believe that Gilgal General has been able to balance the incentives, the respective winners and losers of this shift are:

Winners:

Retirees: Reduced commissions and transaction costs; Buy annuities in minutes, not weeks.

Pension plans: Revenue-sharing; Eliminate fiduciary liability risk due to 2019 SECURE Act.

Insurance companies: Revenue-sharing; Operational cost savings due to automation, digitization, and standardization.

Brokerages: Revenue-sharing.

Losers:

Brokers and investment advisers: Bypassed by technology (as usual).

- Scalable and high margin business model: The technology solution has limited variable costs and should therefore scale well. Gilgal General charges retirees and insurance companies fees for trade execution and takes a 12%-25% cut of all transactions on the exchange. For a good margin comparison, consider NASDAQ’s EBITDA margin, which hovers around 25% and an ROE around 15%.

- Business is self-funded: Alexander holds 100% of the shares in the company and he has self-funded it to date. Like legendary angel investor Jason Calacanis , we get really excited when people have the conviction to invest their own hard-earned cash to fund their vision.

What Makes Us Nervous

- Investors are getting in before proven product-market fit: While it’s impressive that 8 U.S. insurance companies have already agreed to be part of the electronic trading exchange platform and a the company closed a 4 year deal with the InterContinental Exchange for market data, investors should keep in mind that this is a very early stage business with a big, challenging task ahead of it.

- Technology risk: The company is planning to launch a beta version in Q2 2022 followed by a wider release the following year. In other words, there is plenty of time to run into tech-related issues before investors see anything close to a market-ready product.

The Investment

The company offers investors a SAFE with a valuation cap of $9.5 million. You are essentially betting that the company will be worth more than $9.5 million in the future.

We arrive at a max valuation of $9.6 million, suggesting that the company’s valuation is reasonable. Assuming that Gilgal General reaches $72 million in sales in year 5 (equates to a 2.4% market share of SAM) and an EBITDA margin of 25% (2 points less than NASDAQ), a >14x return is possible.

Following its raise on Wefunder, we estimate that Gilgal General will have a cash runway until the end of 2021. So, anyone investing here should assume additional financing rounds with associated dilution.

Please refer to our valuation model for a more in-depth explanation.

As always, if you have any questions or comments regarding the valuation model, please feel free to reach out to our valuation guru Olof on Twitter. He’s good. Real good.

The CAPVEE Call

We view Gilgal General as a buy with >14x Return Potential.

Hit us up on Twitter and let us know what you think! We are always happy to hear from you and discuss your questions and concerns.

Further Reading:

Disclosure: The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a duly licensed professional for investment advice.